It is hard to imagine another industry where trying to count their customers creates as many challenges as it does for credit unions. You are not likely to run into a grocery store that is not sure how many customers they have. And yet, counting members is a challenge for credit unions for a variety of reasons that we will explore in this article.

Who’s a member?

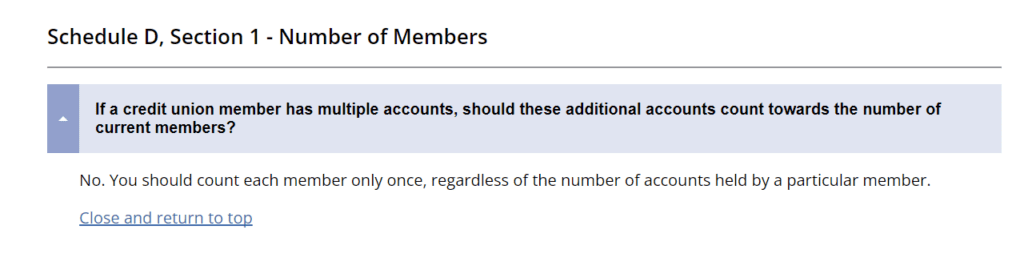

Every Credit Union has to report their membership to the NCUA quarterly on the 5500 call report. NCUA has provided guidance that this number should include only individuals and not be increased by the fact that the individual may have more than one account or membership with the credit union. As a point of reference, further reading from the NCUA.

Just fulfilling this requirement presents several challenges to CUs when trying to count their members. For CUs with a considerable international population who don’t have an SSN, counting accounts may be the only feasible way of counting people. If a member’s SSN is tied to both a personal and a business account, should that person be counted as one or two members? From the above, the NCUA has provided direction that this should be one member, however, does your credit union have business metrics that require them to be counted as two? Should you consider a minimum in their share account, a charge-off, or bankruptcy?

One of the reasons why the CU has trouble defining its members is that different groups have different needs. Each of these groups will use the term ‘members’ but will mean something slightly different. Consider that marketing wants to get to a single person so they don’t send different messages to the same member. The CU’s board wants to know how many members are in good standing, so they will not want to count people who may have caused the credit union a loss. Retail may be interested in new accounts since that is how they compensate their team.

Understanding up front that you need different counts for different purposes will reduce the amount of confusion and disagreement in the CU.

One more challenge in defining a member is that for most CUs, no one group owns the definition. Because of the various relationships each department may have in interacting with or using member information, it is challenging for the credit union to establish a process that effectively stewards the member information in an enterprise-level manner. Credit unions do initiate short-term initiatives to clean up and improve member information across the credit union, but these initiatives lose steam over time due to other initiatives taking priority of credit union staff time and resources. Without an owner, most CUs will never have enough focus to work through the different demands of the different groups, let alone create enough momentum to overcome how they have been reporting to the NCUA for the past 20+ years.

The Value Ratio

CFS Insight has had the good fortune of working with many different CUs regarding their member counts. Let’s take a fictitious CUs member breakdown to help illustrate the point.

In this example, CU has 100k members who are not closed.

-

- Members who have at least $5 in a share 🡪 85K

-

- Members who have at least $5 in a share and had no charge off / bankruptcy 🡪 75k

-

- Members who have at least $5 in a share and no charge and have at least 5 transactions 🡪 50k

-

- Members who have at least $5 in a share and no charge and have at least 15 transactions and have at least $500 in a loan 🡪 20k

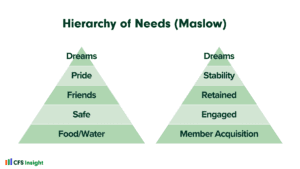

While these numbers are fictitious, they represent a common ratio that we have seen across a number of CUs. Moving from just “not closed” to members who are probably creating value is usually a reduction of at least 8 to 1, but we have seen as far out as 10 to 1. Represented differently, for every 10 members the CU brings in, only 1 will create value for the CU. Knowing this ratio allows the CU to ask a variety of questions about their membership and how to improve it.

Desired Outcome

Most CUs put an enormous effort into tracking what would be considered “members not closed.” They will measure the current total, new members this month or quarter, new members when compared to this period last year, and so forth. But as we have seen, this is a very misleading number and leads to a focus on less valuable aspects of the membership. Perpetually adding more members when the majority are not engaged is probably not an effective use of resources.

The purpose of the CU is to try and create value for as many members as possible. Given that goal, a total count of members is only valuable in the context of using it as a denominator with the valued members to get a ratio.

With the goals of creating value, and not just member count, we can start to look for ways to improve the relationship with the member. We can look at members who maybe only have a loan relationship with the CU and use the transactional records to see where the payments are coming from to create a new share campaign. We can look at members who don’t have a debit card or are not using it and create campaigns to increase its usage. We can look at the share accounts and see where they are making payments for loans at other institutions. All of this data is already available to the CU but is not being harnessed to create more value for both the member and the CU.

Better Measures; Better Outcomes

Knowing the ratio from above, CUs can create counts at different levels that help them understand how many total people they have but also where they are in terms of engagement with the CU. Here are some example measures and why it would be helpful to measure at this level.

| Title | Calculation | Purpose |

|---|---|---|

| Total Accounts | A total count of accounts that are open on the core platform. This includes accounts that are tied to troubled assets as well as accounts for which the original account has passed and may be escheated. | Trial balance calculations of core systems often reconcile based upon the number of memberships opened which is typically a larger number than the list of primary membership or account holders tied to these accounts. |

| Total Entities | Unique count of taxable IDs that have at least one open account | This is helpful to know how many people could walk into a branch |

| Total Members | Unique count of taxable IDs that have an open savings account (or share) in the credit union that constitutes membership in the credit union per the credit union charter. This definition also factors out members who are in bankruptcy, may have caused the credit union a loss or who have passed but their assets have not yet been transferred to their rightful heir. | This is usually the number that gets reported to the NCUA. The process for creating this number is often times manual and falls upon someone in the accounting department or whoever is responsible for reporting membership on the 5500 Call Report. |

| Active Members | Minimum requirements plus >$5 in share and > 5 transactions in the last 30 days | This is important to know how many members have some level of engagement with the CU |

| Valued Members | Active plus >7 debit card transactions | These members are at least generating interchange income and more importantly utilize the credit union services in their day-to-day finances. |

| Peak Members | Valued Members plus they have more than $100 in a loan or an active credit card | These members represent where they have at least one loan and a share with your CU |

First Steps

Getting started can be difficult for many CUs. We recommend a combination of simple measures and ownership.

-

- Defining a primary owner of the member definition will improve the chance of making progress on goals.

-

- For credit unions that are smaller and have a person driven core system, develop a process that gives you valid reporting on the various member types in the table above.

-

- For larger CUs with many interlacing systems, you will want to try and abstract the member definition away from these other systems and into the data warehouse.

-

- If you can’t implement all the membership categories defined above, implement the Total Entities and Members as a first phase and work on the other definitions that move toward an Active, Valued, and Peak members in subsequent phases.

-

- In reporting member numbers, establish a dashboard that reports them in an automated manner for each month but preferably daily. Separate the technology implementation of automating the reporting of member counting/metrics from the business ownership.

-

- Technology ownership – includes the implementation, support and maintenance of the custom reporting, data integration business rules applied to processing the member data deriving the counts with self-service drill down.

-

- Business ownership – includes the documentation and decision of business rules, initial and ongoing validation that counts are accurate. It also includes management and definition of the change that must be made as underlying systems. For example, if the credit union wants to implement a new CRM, the owners of the member numbers should be involved in the implementation.

-

- In reporting member numbers, establish a dashboard that reports them in an automated manner for each month but preferably daily. Separate the technology implementation of automating the reporting of member counting/metrics from the business ownership.

Conclusion

While counting members is challenging, there can be value created beyond just reporting a number to the NCUA. By accepting that different groups have different needs will reduce the friction on member counts. More importantly, looking at member engagement allows the CU to improve the value generated. Assigning a unique ID per member and partnering with the CU to apply its own unique business rules, CFS standardly provides this capability which allows the CU to truly determine their membership count as accurately as possible. Click here to learn more about our data analytics solutions.